By Sachiko Suzuki, Asia Climate and Energy Analyst, Market Forces.

Cover image: LNG-related facilities in which Japan’s INPEX and JERA have stake, are concentrated in Darwin, Australia. (Image credit: Paula Martinez / Market Forces)

According to the Japan Meteorological Agency, the average temperature in Japan from June to August this year was the highest on record. The extreme heat has become more frequent, and the negative impact on the economy is becoming apparent, such as a decline in labor productivity, a decrease in sales, and a rise in crop prices.

It is also estimated that the burden on households will increase by 100,000 to 300,000 yen per year due to “severe heat inflation”.

In order to stop further temperature rise, it is necessary to change the economic and social structure by phasing out the extraction and use of fossil fuels, the largest source of greenhouse gases, which is the cause of climate change.

If we act now, we still have time to mitigate the worst impacts of climate change, but there is little time left.

Managing climate-related financial risks is part of fiduciary duty

It has long been said that the worsening of climate change will lead to chaos in the financial system and the economy as a whole in the future. In other words, “climate risk is financial risk”, and it is a problem that business people cannot overlook.

Market Forces aims to genuinely decarbonise the investment and financing value chain. The organisation has been conducting research and working to help companies maintain their competitiveness by properly responding to risks and opportunities posed by climate change.

Market Forces analysed the amount of stock investment in 190 fossil fuel-related companies around the world and the amount of stock investment in 201 clean energy companies by five major Japanese institutional investor groups (including Sumitomo Mitsui Trust Group, Nippon Life Insurance, Daiichi Life Insurance). The results were published in June.

The analysis revealed that these big Japanese investors held slightly more investment in clean energy companies (about 6.5 trillion yen, as of the end of February 2025) than in fossil fuel-related firms (about 6.1 trillion yen, the same). However, the research found that the Japanese investors surveyed were not meeting the minimum investment ratio required of four times more clean energy than fossil fuels by 2030 to keep the global average temperature rise below 1.5 degrees as estimated by Bloomberg New Energy Finance.

The group of fossil fuel-related companies analysed included companies that plan to expand the extraction or use of fossil fuels in the future. More than 80% of the equity investment by the institutional investors surveyed in these 190 companies expanding fossil fuels was concentrated in 10 companies including Mitsui & Co., Mitsubishi Corporation, and ExxonMobil.

These 10 companies’ plans to expand their fossil fuel projects alone would emit 7.7 billion tons of carbon dioxide (CO2) equivalent of greenhouse emissions. This 7.7 billion tons is comparable to the emissions reduced by installing renewable energy worldwide in the past three or so years. In other words, if these expansion plans go ahead, the cumulative emissions reduction efforts by countries and businesses around the world will be written off instantly.

All the institutional investors surveyed hold assets including pensions, and ultimately owe a fiduciary duty to us citizens.

It is the responsibility of institutional investors to tell the leaders of the investee companies to make sure that the company remains competitive by managing the risks posed by climate change, or to express their intentions to the directors using the voting rights at the shareholders’ meetings. These are important means to fulfill investors’ fiduciary duty.

In addition, corporate leaders, particularly directors, have a fiduciary duty to shareholders and to all of us, the public, because the pension premiums paid by us in Japan are invested in stocks and other assets through institutional investors, we are indirectly company shareholders.

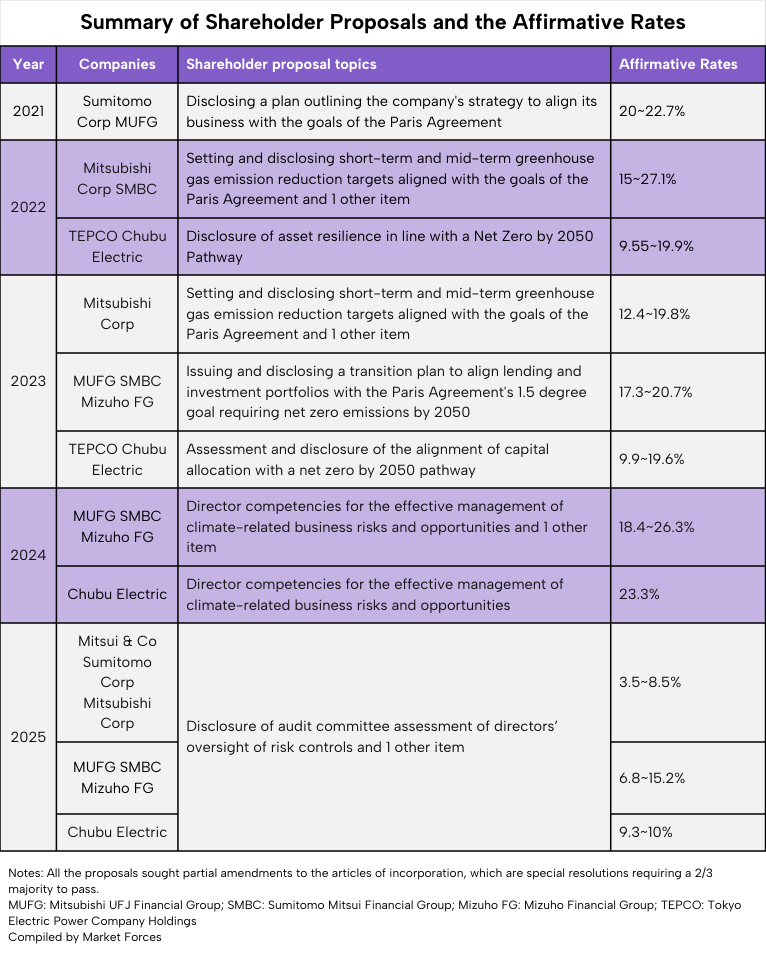

In Japan, since 2021, Market Forces has been filing shareholder proposals to banks, trading houses, and power companies, seeking to enhance information disclosure on financial risk management caused by climate change. All of the target companies have been deeply involved in the extraction, use, or financing of fossil fuels.

The shareholder proposals, proposal contents, and affirmative rates in the past five years are shown in the table below. It shows that our shareholder proposals have gained a significant level of support.

However, filing shareholder proposals is a means, not an end. Some only focus on whether or not shareholder proposals are adopted. However, what matters to Market Forces is the subsequent behavioral change in companies of concern.

So far, banks and trading houses have strengthened policies and set goals for decarbonisation.

For example, Japan’s big three banks have improved their policies to stop financing new expansion of coal-fired power plants and thermal coal mining projects, and committed to bring their greenhouse gas emissions from financing to net zero by 2050.

Sumitomo Corporation also set a time to discontinue its coal-fired power generation business. We believe that the efforts by Market Forces and other stakeholders have influenced these policy improvements and goal setting.

Lack of information on the supervisory function of the board of directors

Enhancing corporate value by effectively managing climate-related financial risks is a consistent theme of Market Forces and its co-filers’ shareholder activism.

For effective management, the shareholder proposals have asked the companies to set and disclose business strategies and emissions reduction targets consistent with the climate goals of the Paris Agreement.

While Market Forces’ shareholder activism has achieved significant results in the phase-out of coal-fired power generation, three megabanks, trading houses, and power companies still finance or invest a significant amount in fossil fuel businesses. This is despite the fact that all of these companies have declared that they would reach net zero greenhouse gas emissions by 2050. Judging from the inconsistency between words and deeds, it is inferred that the management oversight is not fully functioning when making the “Net Zero Declaration” an integral part of the business.

This is a serious problem of corporate governance. It is an issue that corporate leaders and shareholders should work on jointly and responsibly.

Shigeru Nakajima, a lawyer who is familiar with corporate governance, in his book Kaisha to kabunushi no sekaishi, The World History of Companies and Shareholders, points out that the fundamental reason why good corporate governance is not realised is that many corporate leaders lack awareness to seriously fulfill their fiduciary duty to shareholders, and lack attitude to actively incorporate opinions from outsiders, including outside directors.

Mechanisms such as appointing outside directors, auditing by the board of corporate auditors/audit committee/audit and supervisory committee, and self-evaluating the effectiveness of the board of directors, are in place. However, these are only formally introduced. As a result, the information that determines whether corporate governance is actually functioning remains opaque to shareholders.

In 2024, Market Forces and its co-filers filed shareholder proposals at Japan’s big banks and a power company asking whether their boards had competency to perform their duties in order to effectively manage climate-related financial risks.

The companies were reluctant to disclose the evaluation criteria to ensure the competency to perform the duties, but they claimed that their boards were competent. Building on that, in 2025, Market Forces and its co-filers filed proposals asking about the evaluation criteria for auditing the appropriateness of the performance of the duties of directors.

Why is it beneficial for shareholders to know such information? Strengthening corporate governance is not limited to responding to climate change risks, but also leads to better risk management and portfolio management for the entire business. As a result, it contributes to the maintenance and enhancement of corporate value.

Climate risk is financial risk, in the first place, and many companies list this issue as one of the most important management issues. However, it is difficult to see from the outside what criteria are actually used to determine that the risk management system is sufficiently functioning. Acknowledging the secrecy, one expert said that the shareholder proposals seeking to scrutinise and disclose the effectiveness of the board of directors was “an extremely thoughtful approach”.

Fulfill fiduciary duty by seeking change in high-emitting companies

It has been 10 years since the Corporate Governance Code was published in Japan, and formal compliance of corporate governance, such as the number of outside directors and the number of female directors, is being observed. However, the quality of governance, especially the effectiveness of the board of directors, remains an issue.

The Financial Services Agency of Japan is planning to revise the Code by June 2026. And the actions to be taken include strengthening the functions of the board of directors, including corporate auditors. This direction aligns with what was sought in the Market Forces’ shareholder proposals in 2025. Sooner or later, companies will be forced to respond.

This article has dealt with the issue of corporate governance with a focus on climate-related financial risks as an example, but isn’t this a case of one thing shows all?

In other words, if it is a problem in one company, there is a high probability that other companies have the same issue. In particular, the companies this article focuses on are leading firms in the Japanese market. As a result, the problem of corporate governance could undermine the system-level, or the whole market, and competitiveness of the economy and stable growth.

If that happens, the source of the pension we will receive in the future will also shrink. Now is the time for institutional investors to enhance dialogue with investee companies and show their intentions through their votes at annual meetings, in order to change the course of high-emitting companies.

Otherwise, investors will not be meeting their fiduciary duty, and risk their reputation, and endanger the assets of the citizens who are the ultimate beneficiaries. It is nothing but exposing the economy and people to the devastating effects of climate change. Institutional investors bear a massive responsibility, just like corporate leaders.

First published in Toyo Keizai Online. Note: this version differs slightly from the Japanese version as it appears in Toyo Keizai Online.